Canada’s Fighting Against Forced Labour and Child Labour in Supply Chains Act (“Modern Slavery Act”) came into force on January 1, 2024, creating new transparency requirements for many companies that import, produce, sell, or distribute goods in Canada. The deadline for the first reports is May 31, 2024.

Without question, modern slavery legislation – which broadly creates requirements relating to severe human rights abuses – represents an increasingly significant global regulatory trend. What are the similarities and differences between Canada’s new Act and modern slavery legislation in other jurisdictions, and what are the implications for companies and investors?

What is “Modern Slavery”?

There is no single clear definition of “modern slavery.” While terms like “modern slavery,” “modern-day slavery,” and “contemporary forms of slavery” are widely used, they may be defined and applied in different ways. Generally, however, modern slavery is used as an umbrella term that encompasses various forms of exploitation of others for personal and/or commercial gain such as forced labour, debt bondage, human trafficking, sex trafficking, exploitation of children, and forced marriage.

Forced labour and child labour, which are the focus of Canada’s new Act, are global problems prevalent in both low-income and high-income countries: the 2021 Global Estimates of Modern Slavery found that 27.6 million people were in situations of forced labour, while UNICEF’s most recent Child Labour Report revealed that the number of children involved in child labour had risen to 160 million worldwide.

Under Canada’s Act, entities required to report must disclose the steps taken, if any, to assess and mitigate the risk of forced labour and child labour in their supply chain. They must prepare a report with approval and attestation by their governing body, complete a mandatory online questionnaire, upload the report, and publish it on their own website. The Act does not mandate specific due diligence activities. Nor does it include prohibitions on modern slavery, which are covered by other statutes such as the Criminal Code.

While the Act is a landmark piece of legislation in the Canadian context, some provisions will be broadly familiar to companies and investors already reporting under similar requirements in other jurisdictions that have adopted modern slavery-related disclosure requirements, including Australia, California, France, and the United Kingdom.

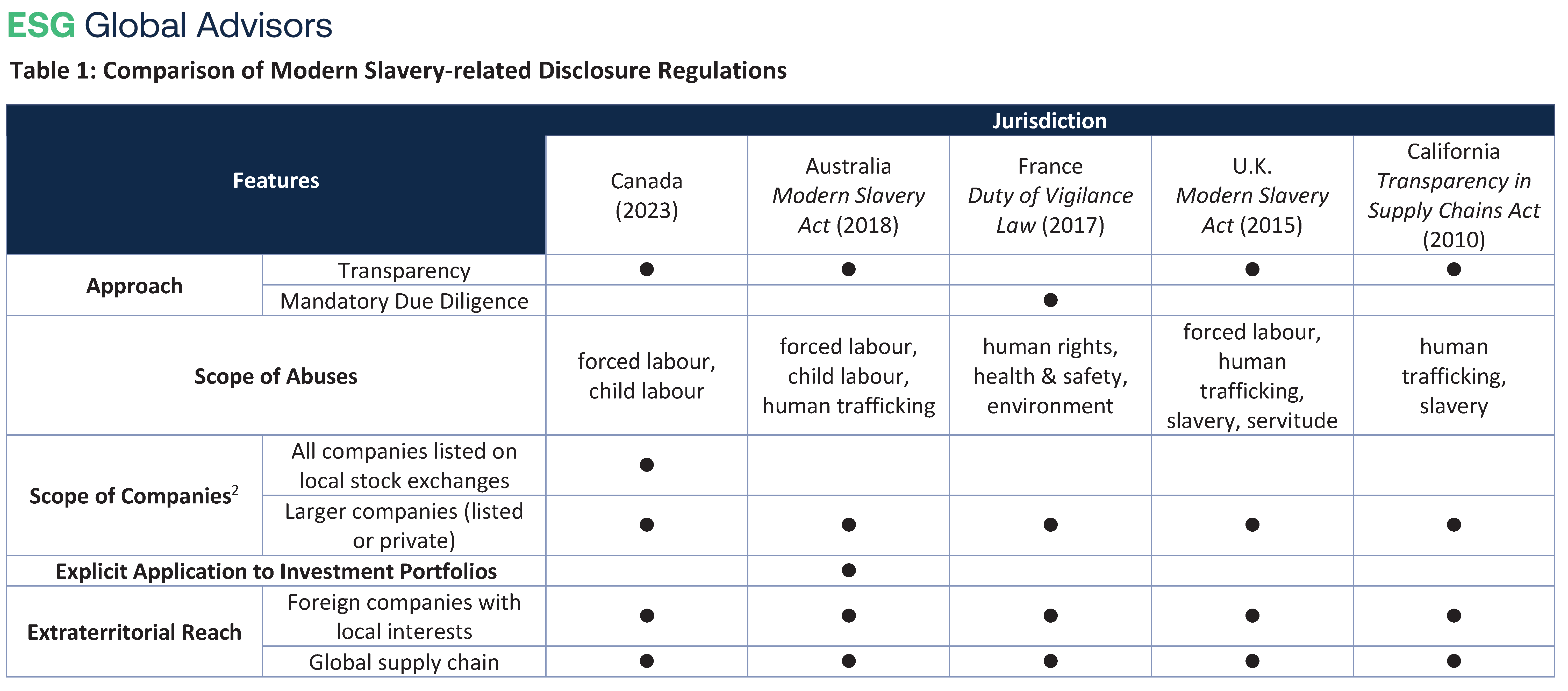

How do regulatory responses differ across jurisdictions? Below we outline some key features that are helpful for navigating the global landscape of modern slavery legislation.

Transparency vs. Mandatory Due Diligence: Regulatory responses generally follow one of two approaches: requiring companies to report if they are addressing modern slavery risk in the supply chain, and if so, to report on the approach and results (a “transparency approach”); or requiring that companies must investigate modern slavery risk in the supply chain and report on the approach and results (a “mandatorydue diligence approach”). Canada’s Act follows a transparency approach, while the French Duty of Vigilance Law follows a mandatory due diligence approach. There is some inherent overlap since both approaches require companies to make disclosures. The key distinction is that a transparency approach does not impose the requirement to undertake specific actions to combat modern slavery. (For more information on corporate responsibility due diligence, see the callout below – “OECD Due Diligence for Responsible Business Conduct”.)

Scope of Abuses: Because modern slavery is not clearly defined by international convention, regulations address differing scopes of human rights abuses. For example, Canada’s Act has a narrow focus on child and forced labour, while at the other end of the spectrum the French legislation covers a wide scope of potential adverse impacts for human rights, health and safety, and the environment.

Scope of Companies: The types of entities required to report may differ across jurisdictions. At a high level, modern slavery disclosure regulation tends to apply to larger companies, both listed and private, although the criteria by which “size” is determined can vary (e.g., revenue, turnover, number of employees). The scope of sectors and business activities covered may be broad or narrow: for example, California’s regulation only applies to retailers, sellers, and manufacturers, while the U.K. Modern Slavery Act applies to companies providing both goods and services. Notably, under Canada’s Act, all companies listed on Canadian stock exchanges that import, produce, sell, or distribute goods are potentially in scope, regardless of size.1

Explicit Application to Investment Portfolios: Regulations differ as to whether investors are expected to report on measures to address modern slavery risk in the supply chain of portfolio companies. For example, the guidance for Australia’s Modern Slavery Act explicitly calls for high-level reporting in relation to investment and lending portfolios, while the requirement in Canada’s Act for entities to report where they have “control” of another in-scope entity could potentially capture investors with a majority stake.

Extraterritorial Reach: Modern slavery regulation typically covers not only companies based in the relevant jurisdiction, but also foreign companies with subsidiaries or significant business interests there. In addition, reporting requirements typically cover the global supply chain of companies, not just the supply chain leading into the jurisdiction.

Based on these features, Table 1 compares Canada’s Act with modern slavery disclosure regulations in Australia, California, France, and the United Kingdom. 2

Click table to expand

OECD Due Diligence for Responsible Business Conduct

The Organization for Economic Cooperation and Development (OECD) Guidelines for Multinational Enterprises on Responsible Business Conduct is an international corporate responsibility framework endorsed by over 50 countries including the U.S. and Canada. A key element is risk-based due diligence to assess and address environmental and social impacts of a company’s operations and value chain, including investment and lending portfolios. The OECD due diligence approach influences regulation globally, and is cited in official guidance for Canada’s Act.

What are the Penalties Under Canada’s New Act?

Across the global regulatory responses to modern slavery, the extent to which penalties for non-compliance are specified, and the severity of these penalties, varies significantly. For example, there is no legal sanction associated with non-disclosure under Australia’s Modern Slavery Act, which takes a “name and shame” approach, while the administering authorities under the California and U.K. legislation may seek an injunction.

Under Canada’s Act, entities or individuals that fail to meet the reporting requirements can face specific penalties:

Offence: An entity or person that fails to comply can be guilty of an offence punishable on summary conviction and liable to a fine of up to C$250,000.

False or misleading statement or information: Every person or entity that knowingly makes any false or misleading statement or knowingly provides false or misleading information to the Minister is guilty of an offence punishable on summary conviction and liable to a fine of not more than $250,000.

Liability of directors and officers: Every director or officer or agent or mandatary of the person or entity who directed, authorized, assented to, acquiesced or participated in its commission is a party to and guilty of the offence and liable on conviction to the punishment provided for the offence, whether or not the person or entity has been prosecuted or convicted.

Implications for Companies and Investors

As Canada’s Act comes into force, here are five implications for companies and investors:

The penalties under the Act are for failing to provide timely, truthful, and transparent disclosure, not for failing to establish a strong due diligence process, or for the actual presence of forced labour or child labour in the supply chain. A company disclosing that it has not yet implemented a robust supply chain due diligence process could still be in compliance with the Act. Over time, however, disclosing weak due diligence is likely to become an increasing reputational risk, especially if peer companies and competitors enhance their disclosure. Furthermore, in an evolving global regulatory landscape, companies may eventually find themselves subject to mandatory due diligence requirements – either because their home jurisdiction has adopted this approach, or because international business activities bring them into the scope of regulation in another jurisdiction. Mandatory due diligence requirements are an emerging trend: for example, in May 2023 the Australian Government outlined recommendations for reform of its Modern Slavery Act, including new mandatory due diligence requirements.

While companies already reporting under legislation in other jurisdictions will have a head start complying with Canada’s Act, requirements are not uniform. Aligning with internationally-recognized due diligence frameworks, such as the OECD guidance, can help companies to position for the future. (For more information on corporate responsibility due diligence, see the callout above – “OECD Due Diligence for Responsible Business Conduct”.)

While some companies already have mature policies and practices that address modern slavery, others may need to invest significant effort in exploring supply chain risk and developing due diligence. In this context, it is important to note that the Act focuses on how workers in the supply chain are exposed to forced labour and child labour risk – not whether these abuses present risk to the company’s financial performance. As a result, some companies required to provide disclosure under the Act may not have identified modern slavery as a material factor in earlier ESG materiality assessments and may need to undertake additional supply chain-focused risk analysis.

The Act requires the company’s governing body to approve its modern slavery disclosure. There are already increasing expectations that a company’s board of directors should provide and disclose on oversight of material ESG factors – expectations that are reflected in ESG disclosure frameworks and in the voting guidelines of proxy advisors. Boards may need to update ESG governance mandates, structures, processes, and skills to respond to duties created by the Act.

Companies can fall under the scope of the Act if they undertake relevant activities or control companies that undertake them. In this context, one remaining area of uncertainty surrounds expectations for institutional investors to disclose in relation to portfolio companies where they hold a controlling stake.

The modern slavery regulatory environment presents challenges for companies and investors, especially for those operating in multiple jurisdictions with differing requirements. In Canada, despite publication of official guidance in December 2023, lack of awareness and confusion persists. What is certain, however, is that supply chain concerns have moved up the Canadian ESG agenda.

How Can Companies Prepare?

With the deadline for first reports under Canada’s Act fast approaching, companies with Canadian interests should act now to determine if, and what, they need to disclose. Here are four actions companies can take to integrate supply chain considerations into their ESG program:

Review current supply chain risks and practices: Entities that fall within the scope of the legislation should review current exposure to the risk of child and forced labour in the value chain as well as current procurement practices, and the extent to which they include due diligence measures that address child and forced labour.

Prepare modern slavery disclosures: Entities will need to produce an annual report and complete an online questionnaire. To avoid exposure to penalties under Act, it is important to ensure the accuracy of information disclosed and to avoid false or misleading statements. Depending on the structure of the entity, collecting the required information may take time.

Board training: Since the board needs to sign off on annual modern slavery disclosure, directors may need training to feel comfortable providing the necessary approvals. Enhancing director understanding of supply chain risks and opportunities will be an important component of future board education programs, as due diligence expectations are only likely to increase over time.

Supply chain strategy development: Looking beyond the first-year reports that are due May 31, 2024, it is important to prepare for future reporting by developing a strategy to reduce supply chain risk over the longer term, including integration of supply chain audits, policies, and due diligence measures to existing procurement practices. While the Act focuses solely on the issues of child and forced labour, to reduce risk and ensure alignment with broader ESG strategy it will also be important to integrate other material ESG issues into supply chain strategy, such as emissions management.

Need help with supply chain reporting and supply chain strategies, aligned to your ESG program? ESG Global offers a comprehensive range of ESG services for companies and investors. Visit Our Services to learn more.

Disclaimer: Please note that the content and material provided in this article is for general information purposes only. It is not to be taken or relied upon as legal advice and should not be used for professional or commercial purposes. This article is intended to communicate general information about relevant sustainability matters and reporting requirements as of the indicated date. The content is subject to change based on evolving regulatory reporting requirements.

The drafting in the Act created some ambiguity as to whether listing alone created a potential requirement to report, but this point has been clarified by recent official guidance ↩︎

Canada’s Act applies to “entities,” described as a corporation or a trust, partnership, or other unincorporated organization, that engages in the any of the following activities: 1) Produce, sell, or distribute goods in or outside Canada, 2) Import goods produced outside of Canada, or 3) Controls an entity engaged in either of the above activities. ↩︎